Recent natural disasters have served as a timely reminder of the increasing value of insurance-linked securities (ILS) to the global re/insurance market [1]. The ILS market has expanded rapidly since 2012 and now contributes nearly $100 billion (~20%) of additional capacity to the global reinsurance marketplace [2].

The ILS asset class offers capital market investors a mechanism to provide new capital to the re/insurance sector and satisfy the increasing requirement of insurers and reinsurers to reduce risk on their balance sheets while continuing to provide protection to the areas of the world with the greatest demand for insurance – known as the ‘peak peril’ zones.

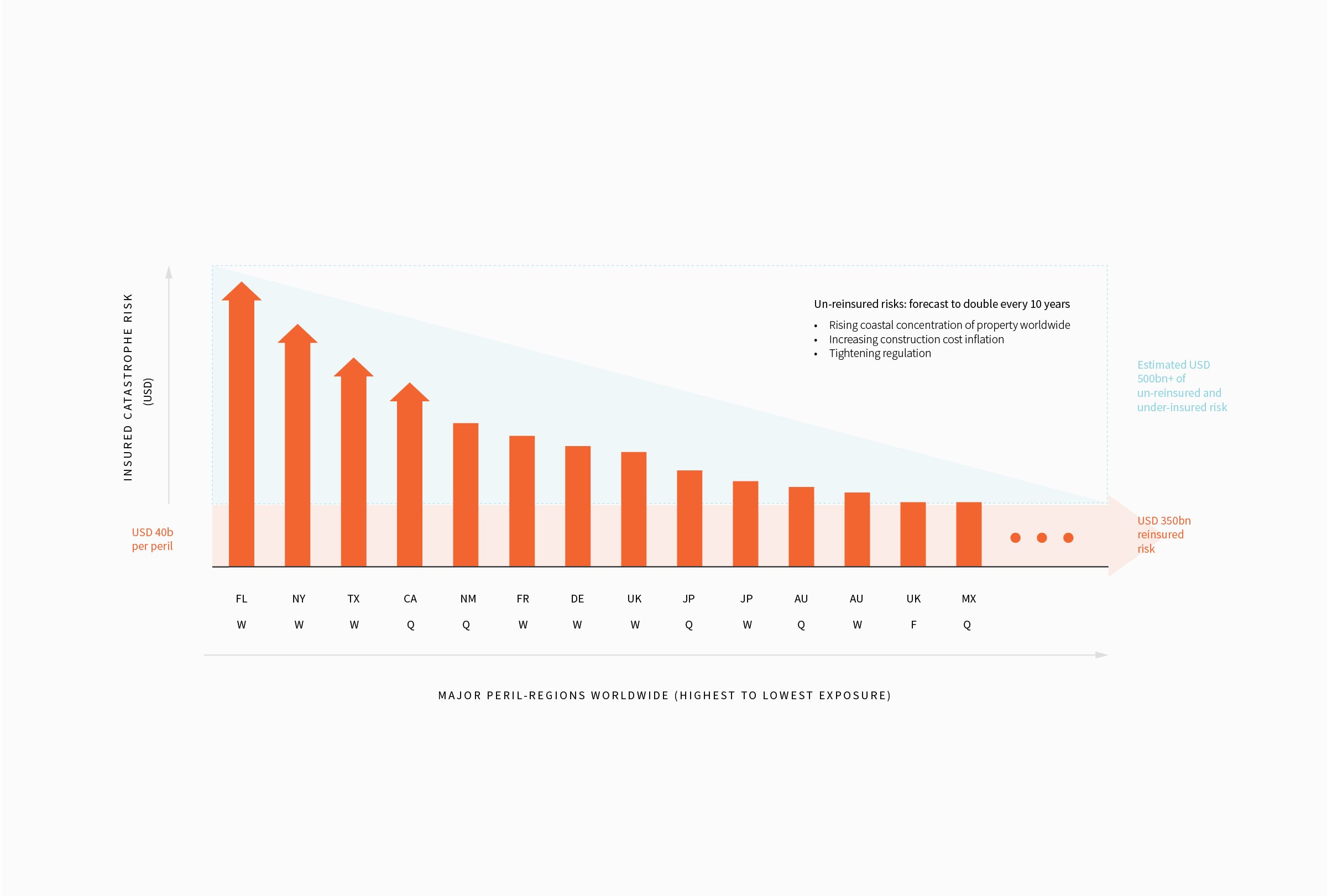

ILS returns are driven by increasing demand for insurance in urban and coastal areas. These areas are undergoing intense population, wealth, and property growth, which accelerates their exposure to both natural and man-made disasters. In some of the largest peak peril zones – states on the U.S. coastline at risk to hurricanes – the insured value of properties, and therefore potential insured losses, have historically doubled every 10 years [3]. However, in the past decade, the total global reinsurance base – the pool of capital available to backstop insurance companies – only increased by an estimated 31% to reach $350 billion in 2018 [4],[5]. Due to regulatory pressures, this total global reinsurance capacity is spread roughly equally across insured risk exposures, with only approximately $40 billion of reinsurance capital available for any given peril [6]. In contrast, one large catastrophe – such as a Category 5 storm hitting the most concentrated property exposures of Miami directly – could cause insured losses exceeding $250 billion in just one event [7]. It is clear that the re/insurance industry is under-prepared to meet the cost of remote but potentially devastating catastrophic disasters.

Pressure on the insurance system is also creating significant “protection gaps”. Even in the United States, the most developed insurance market in the world, only 20% of households affected by Hurricane Harvey flooding in 2017 had flood insurance [8]. Less than 30% of the economic losses of Hurricane Florence in 2018 were insured [9]. The catastrophe events of 2017 and 2018 highlighted not only the mismatch between the capital of the re/insurance industry and potential insured losses from future disasters, but also the large discrepancy between economic and insured losses when disasters do occur. This growing ‘disaster gap’ – composed of under-insured risks as well as insured but un-reinsured risks – is estimated at over $500 billion [10] and is unserviceable by traditional re/insurance mechanisms.

While different in form, ILS instruments – catastrophe (cat) bonds, collateralized reinsurance, industry loss warranties, and sidecars – function similarly to traditional reinsurance. They offer investors a return in exchange for accepting a share of risk exposures from defined insured events – such a hurricanes, earthquakes or, more recently, wildfires. In the absence of major catastrophes, investors receive an inherently stable yield with a low correlation to traditional financial markets.

As economies continue to grow, and as concerns about climate change increase, the gap between insurance needs and available capital will amplify further. ILS reduce this gap, helping to alleviate the financial burden of recovery and rebuilding from these disasters otherwise borne by governments, businesses, and individuals.

In addition to re/insurers, ILS are increasingly being used by companies and governments to manage the cost of extreme risk events. Two examples of this are the U.S. Federal government through the National Flood Insurance Program’s catastrophe bond issuance platform first launched in mid-2018 [11] and the World Bank, which now directly issues catastrophe bonds on behalf of countries seeking to manage their disaster risk proactively [12].

ILS instruments currently only penetrate a small fraction of the risks in the disaster gap today, but with limited new capital formation within the traditional reinsurance sector, the dynamics are set for substantial ILS market growth ahead. As economies continue to grow, and as concerns about climate change increase, the gap between insurance needs and available capital will amplify further. ILS can reduce this gap, helping to alleviate the financial burden of recovery and rebuilding from these disasters otherwise borne by governments, businesses, and individuals. They represent a valuable and growing source of structural capital to this world problem, helping to protect the homes and livelihoods of people around the world and building more disaster-resilient societies. In return for accepting a share of the disaster gap solution, ILS investors can have a measurable beneficial impact on the quality of people’s lives while generating attractive risk-adjusted returns with the added benefit of genuine diversification from more traditional markets.

ILS filling the large gap left by the reinsurance industry.

Peril-region key: FLW, U.S. Southeast hurricane; NYW, U.S. Northeast hurricane; TXW, U.S. Gulf Coast hurricane; CAQ, California earthquake; NMQ, U.S. Central earthquake; FRW, French windstorm; DEW, German windstorm; UKW, UK windstorm; JPQ, Japanese earthquake; JPW, Japanese typhoon; AUQ, Australian earthquake; AUW, Australian cyclone; UKF, UK flood; MXQ, Mexico earthquake.

Source: Fermat Capital Management, LLC, Applied Insurance Research, Guy Carpenter, Aon Benfield Securities. For illustrative purposes only. Diagram is incomplete and not to scale.

ILS filling the large gap left by the reinsurance industry.

Peril-region key: FLW, U.S. Southeast hurricane; NYW, U.S. Northeast hurricane; TXW, U.S. Gulf Coast hurricane; CAQ, California earthquake; NMQ, U.S. Central earthquake; FRW, French windstorm; DEW, German windstorm; UKW, UK windstorm; JPQ, Japanese earthquake; JPW, Japanese typhoon; AUQ, Australian earthquake; AUW, Australian cyclone; UKF, UK flood; MXQ, Mexico earthquake.

Source: Fermat Capital Management, LLC, Applied Insurance Research, Guy Carpenter, Aon Benfield Securities. For illustrative purposes only. Diagram is incomplete and not to scale.

References:

[1] In this note we use the term re/insurance to refer collectively to insurance companies and reinsurance companies.

[2] Sources: “Reinsurance: Will Investor Losses Lead to a Rising Tide for Pricing?” by A.M. Best, 2019 (http://www3.ambest.com/bestweekpdfs/sr705410119549full.pdf) and “Reinsurance Market Outlook” by Aon, January 2019 (http://thoughtleadership.aonbenfield.com//Documents/20190104-ab-analytics-rmo-january.pdf)

[3] Source: “The Growing Value of U.S. Coastal Property at Risk” by AIR, April 2015 (https://www.air-worldwide.com/Publications/AIR-Currents/2015/The-Growing-Value-of-U-S--Coastal-Property-at-Risk/)

[4] Source for total traditional reinsurance capital base growth: “Reinsurance Market Outlook” by Aon, January 2019 (http://thoughtleadership.aonbenfield.com//Documents/20190104-ab-analytics-rmo-january.pdf)

[5] Source for dedicated traditional reinsurance capital: “Reinsurance: Will Investor Losses Lead to a Rising Tide for Pricing?” by A.M. Best, 2019 (http://www3.ambest.com/bestweekpdfs/sr705410119549full.pdf)

[6] Source: Fermat Capital Research

[7] Source: “The 100 Year Hurricane, Karen Clark & Company” by KCC White Paper, June 2014 (http://www.karenclarkandco.com/news/publications/pdf/KCC_Industry_Exposure_Report.pdf)

[8] https://www.insurancejournal.com/news/southcentral/2018/07/31/496541.htm

[9] http://www.artemis.bm/blog/2018/11/05/hurricane-florence-may-cost-n-c-17bn-but-as-little-as-27-insured/

[10] Source: Fermat Capital Research

[12] http://treasury.worldbank.org/en/about/unit/treasury/ibrd/ibrd-capital-at-risk-notes

Last Updated June 2019